Registered S3 method overwritten by 'quantmod':

method from

as.zoo.data.frame zoo

library(TSA)

Registered S3 methods overwritten by 'TSA':

method from

fitted.Arima forecast

plot.Arima forecast

Attaching package: 'TSA'

The following objects are masked from 'package:stats':

acf, arima

The following object is masked from 'package:utils':

tar

library(readxl)library(tseries)

8.2 Definir directorio y leer datos

# Cambiar "\" por "/" en la ruta#setwd("C:/Users/cubid/Desktop/QUARTO - MATERIAS UNAL/9 SERIES DE TIEMPO/Lesson04")# Leer datos desde Exceldatos <-read_excel("Programa_2_datos.xls", sheet ="Datos")

8.3 Preparación de la serie y gráfica inicial

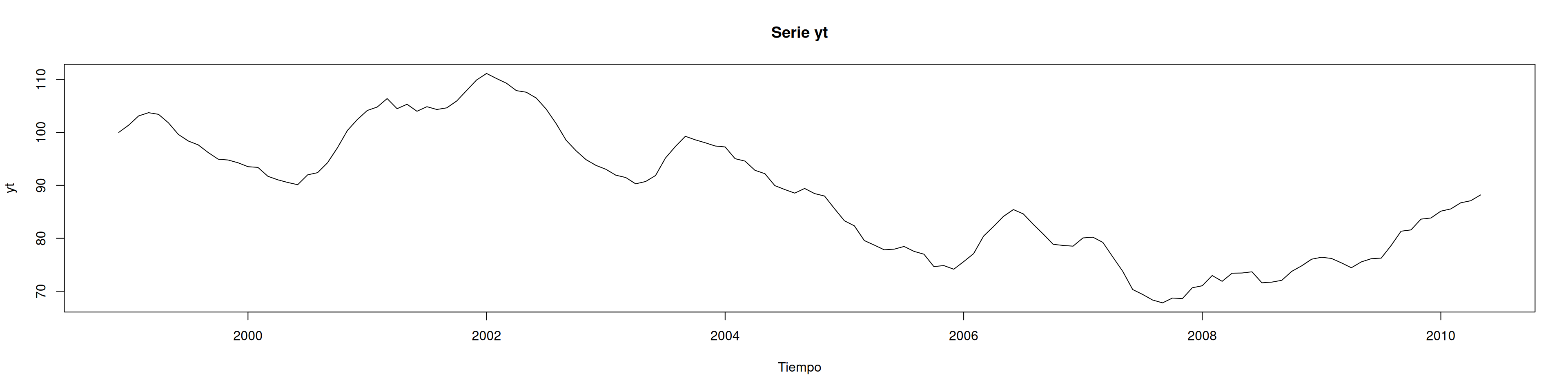

yt <-ts(datos[,2], start =c(1998, 12), frequency =12)plot(yt, type ="l", main ="Serie yt", xlab ="Tiempo")

8.4 Transformación logarítmica para estabilizar varianza

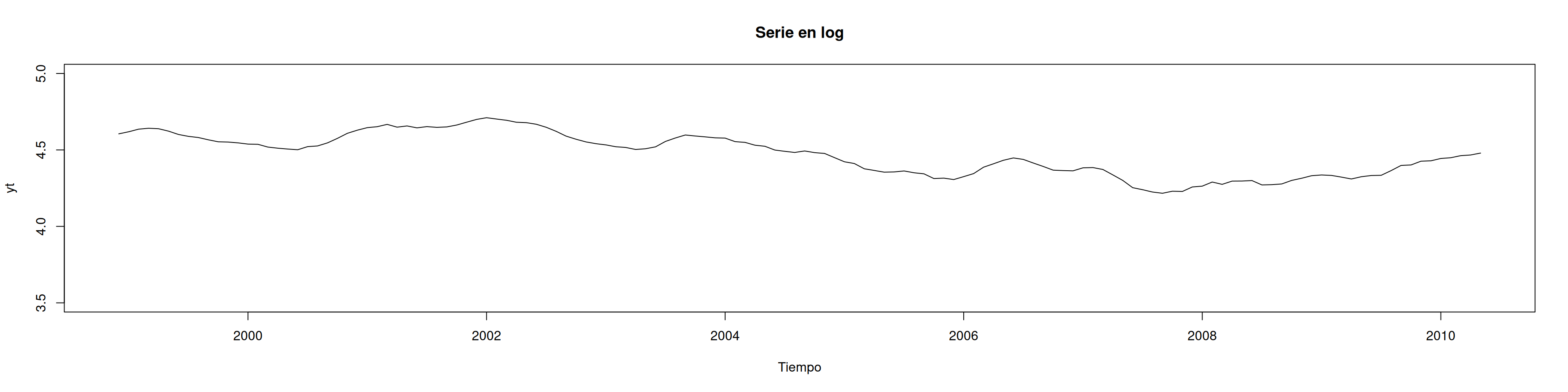

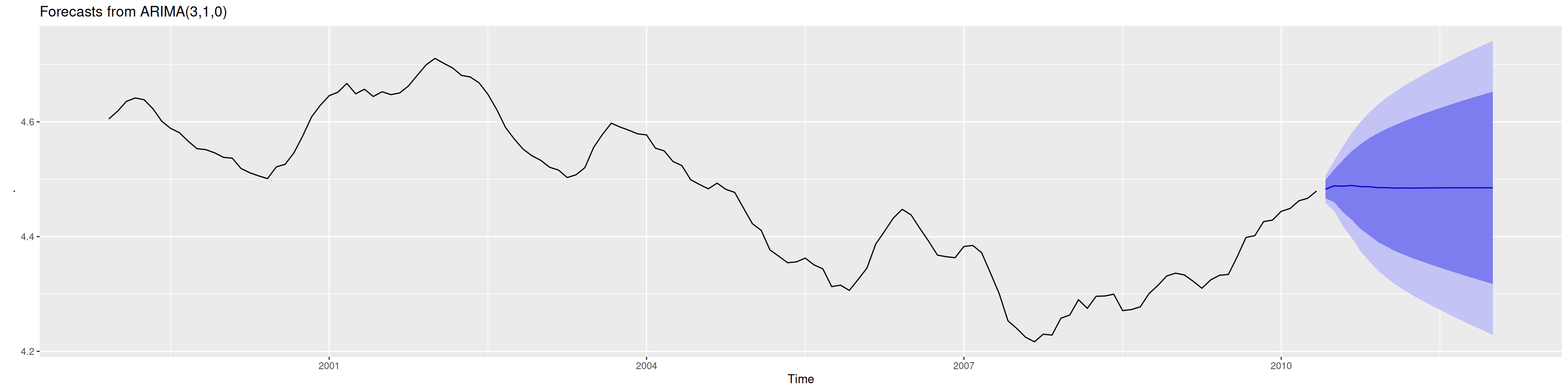

ln.yt <-log(yt)plot(ln.yt, type ="l", main ="Serie en log", xlab ="Tiempo", ylim =c(3.5,5))

8.5 Prueba de raíz unitaria (ADF)

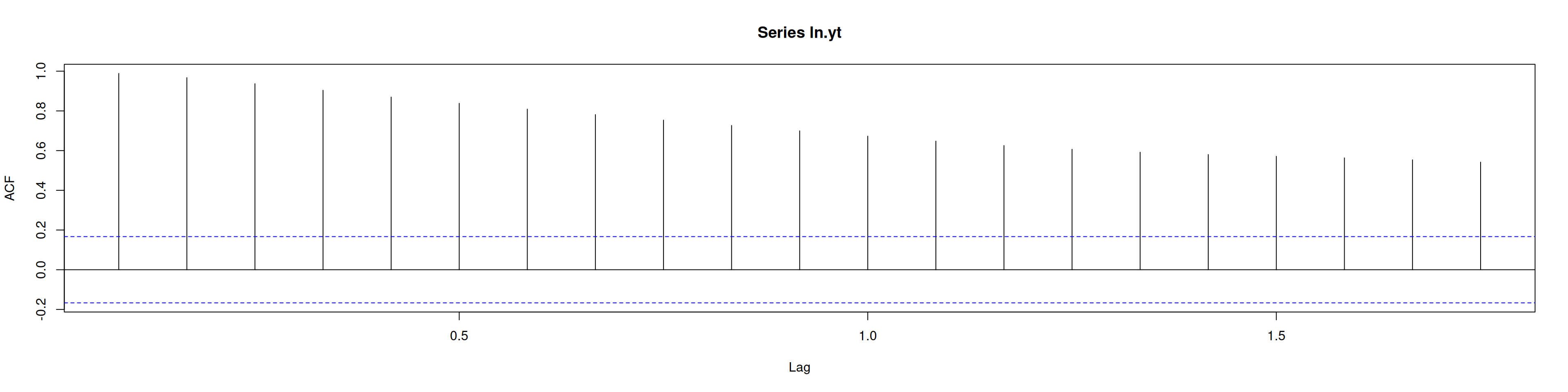

acf(ln.yt)

adf.test(ln.yt) # Ho: no estacionaria, p-valor>0.05 => no rechaza Ho

Augmented Dickey-Fuller Test

data: ln.yt

Dickey-Fuller = -1.4429, Lag order = 5, p-value = 0.8083

alternative hypothesis: stationary

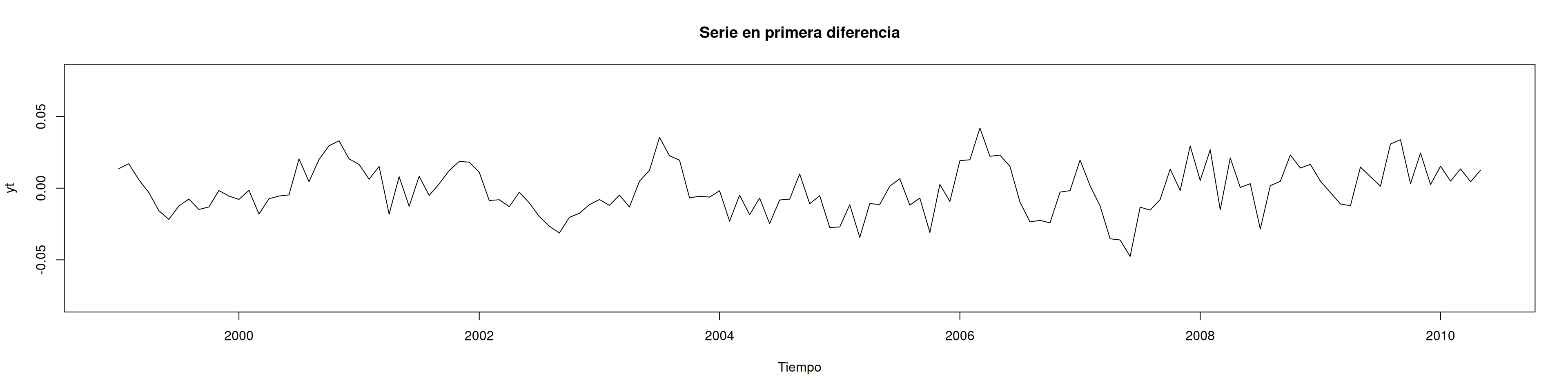

8.6 Primera diferencia para estacionariedad

ytd <-diff(ln.yt, 1)mean(ytd)

[1] -0.000917174

plot(ytd, type ="l", main ="Serie en primera diferencia", xlab ="Tiempo", ylim =c(-0.08,0.08))

adf.test(ytd) # p-valor<0.05 => rechaza Ho

Augmented Dickey-Fuller Test

data: ytd

Dickey-Fuller = -3.9839, Lag order = 5, p-value = 0.01215

alternative hypothesis: stationary

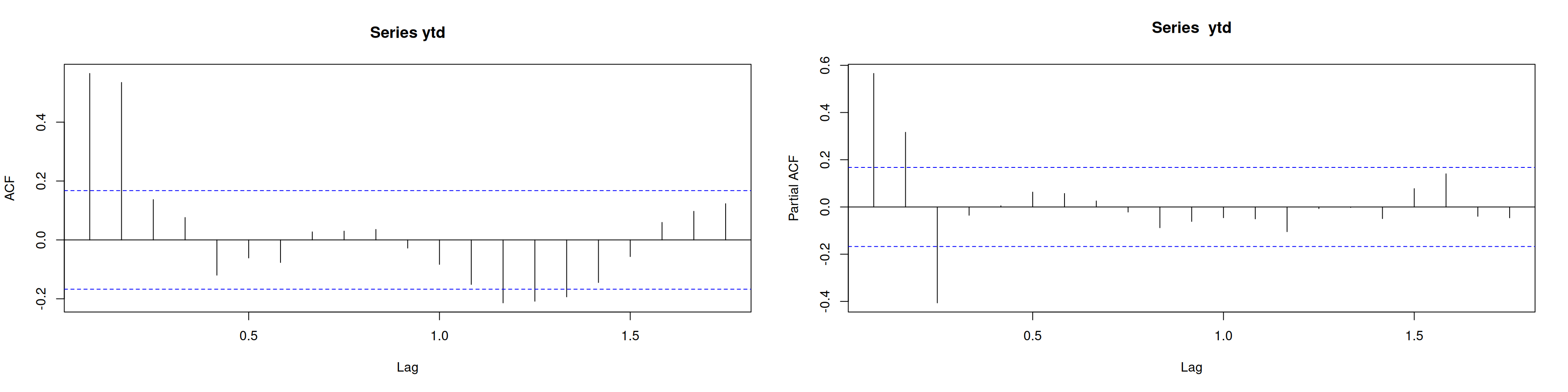

8.7 Identificación: ACF y PACF

par(mfrow =c(1,2))acf(ytd)pacf(ytd)

8.8 Selección de modelo ARMA(p,q)

eacf(ytd) # sugerencia ARMA(3,0)

AR/MA

0 1 2 3 4 5 6 7 8 9 10 11 12 13

0 x x o o o o o o o o o o o x

1 x x x o x o o o o o o o o o

2 x x o x x o o o o o o o o o

3 o o o o o o o o o o o o o o

4 o o o o o o o o o o o o o o

5 o x o o o o o o o o o o o o

6 x x x o o o o o o o o o o o

7 x x x x o o o o o o o o o o

auto.arima(ytd, trace=TRUE)

ARIMA(2,0,2)(1,0,1)[12] with non-zero mean : -798.6118

ARIMA(0,0,0) with non-zero mean : -723.2355

ARIMA(1,0,0)(1,0,0)[12] with non-zero mean : -772.0796

ARIMA(0,0,1)(0,0,1)[12] with non-zero mean : -745.8382

ARIMA(0,0,0) with zero mean : -724.8982

ARIMA(2,0,2)(0,0,1)[12] with non-zero mean : -800.6425

ARIMA(2,0,2) with non-zero mean : -802.8645

ARIMA(2,0,2)(1,0,0)[12] with non-zero mean : -800.6425

ARIMA(1,0,2) with non-zero mean : -801.1236

ARIMA(2,0,1) with non-zero mean : -798.6628

ARIMA(3,0,2) with non-zero mean : -805.3278

ARIMA(3,0,2)(1,0,0)[12] with non-zero mean : -803.1612

ARIMA(3,0,2)(0,0,1)[12] with non-zero mean : -803.1816

ARIMA(3,0,2)(1,0,1)[12] with non-zero mean : -801.9988

ARIMA(3,0,1) with non-zero mean : -807.5113

ARIMA(3,0,1)(1,0,0)[12] with non-zero mean : -805.3912

ARIMA(3,0,1)(0,0,1)[12] with non-zero mean : -805.4143

ARIMA(3,0,1)(1,0,1)[12] with non-zero mean : -804.2908

ARIMA(3,0,0) with non-zero mean : -809.47

ARIMA(3,0,0)(1,0,0)[12] with non-zero mean : -807.3684

ARIMA(3,0,0)(0,0,1)[12] with non-zero mean : -807.3896

ARIMA(3,0,0)(1,0,1)[12] with non-zero mean : -806.3672

ARIMA(2,0,0) with non-zero mean : -786.8746

ARIMA(4,0,0) with non-zero mean : -807.5229

ARIMA(4,0,1) with non-zero mean : Inf

ARIMA(3,0,0) with zero mean : -811.5348

ARIMA(3,0,0)(1,0,0)[12] with zero mean : -809.4548

ARIMA(3,0,0)(0,0,1)[12] with zero mean : -809.4724

ARIMA(3,0,0)(1,0,1)[12] with zero mean : -808.3412

ARIMA(2,0,0) with zero mean : -788.9918

ARIMA(4,0,0) with zero mean : -809.607

ARIMA(3,0,1) with zero mean : -809.5951

ARIMA(2,0,1) with zero mean : -800.805

ARIMA(4,0,1) with zero mean : Inf

Best model: ARIMA(3,0,0) with zero mean

Series: ytd

ARIMA(3,0,0) with zero mean

Coefficients:

ar1 ar2 ar3

0.5166 0.4765 -0.4043

s.e. 0.0772 0.0790 0.0774

sigma^2 = 0.0001495: log likelihood = 409.92

AIC=-811.84 AICc=-811.53 BIC=-800.16

8.9 Estimación de dos modelos

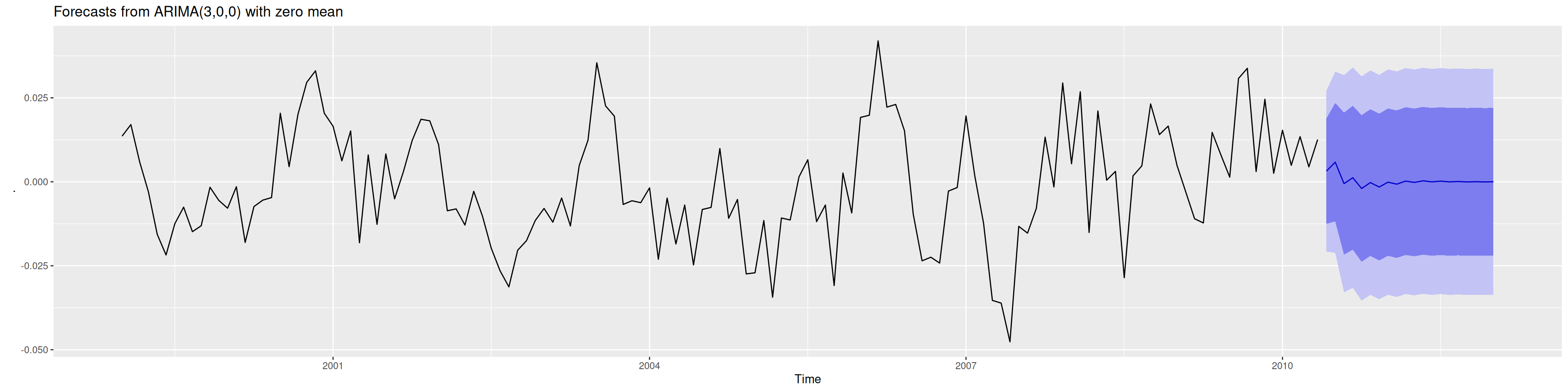

mod1 <-Arima(ytd, order =c(3,0,0), include.mean =FALSE)summary(mod1)

Series: ytd

ARIMA(3,0,0) with zero mean

Coefficients:

ar1 ar2 ar3

0.5166 0.4765 -0.4043

s.e. 0.0772 0.0790 0.0774

sigma^2 = 0.0001495: log likelihood = 409.92

AIC=-811.84 AICc=-811.53 BIC=-800.16

Training set error measures:

ME RMSE MAE MPE MAPE MASE

Training set -0.0003684491 0.01209189 0.009562996 39.69704 126.5415 0.4781506

ACF1

Training set -0.01678247

mod2 <-Arima(ytd, order =c(2,0,1), include.mean =FALSE)summary(mod2)

Series: ytd

ARIMA(2,0,1) with zero mean

Coefficients:

ar1 ar2 ma1

-0.0941 0.6311 0.5533

s.e. 0.1002 0.0704 0.1114

sigma^2 = 0.000162: log likelihood = 404.55

AIC=-801.11 AICc=-800.81 BIC=-789.43

Training set error measures:

ME RMSE MAE MPE MAPE MASE

Training set -0.0002526163 0.01258662 0.01008932 37.02357 119.4948 0.5044668

ACF1

Training set 0.08053776

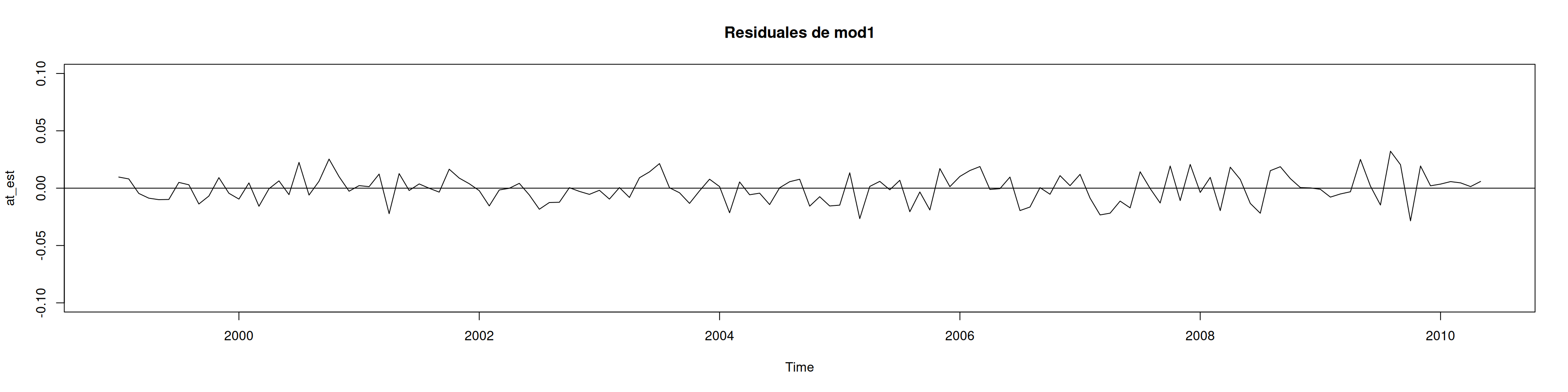

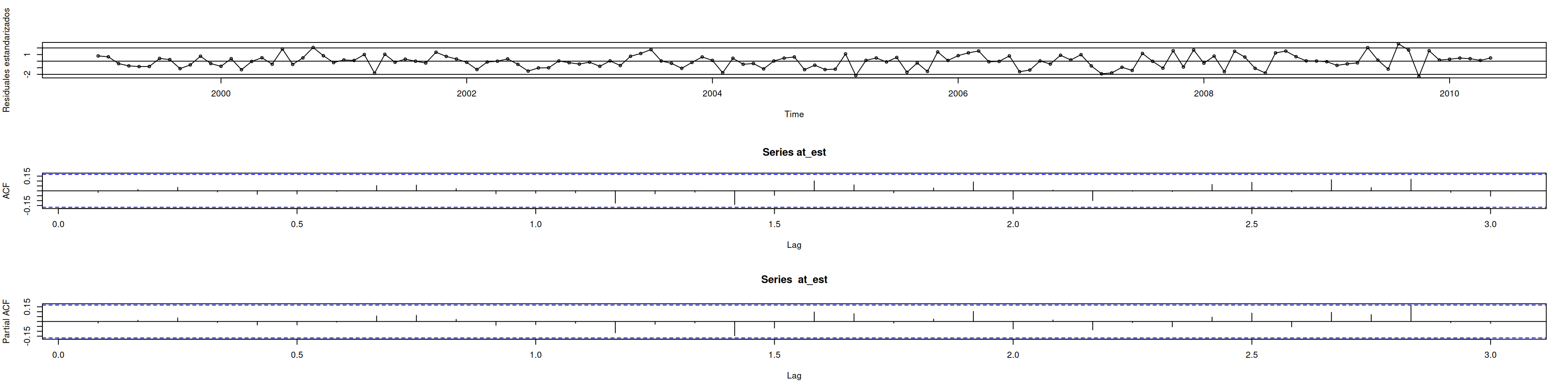

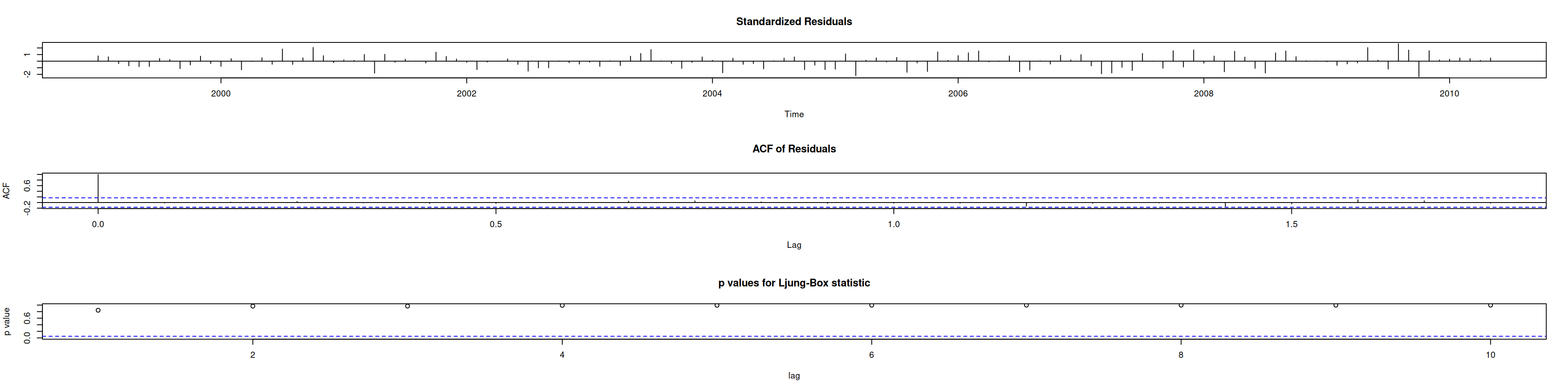

8.10 Diagnóstico del modelo 1

at_est <-residuals(mod1)# Residuales y residuales estandarizadosplot(at_est, ylim =c(-0.1,0.1), main ="Residuales de mod1"); abline(h=0)

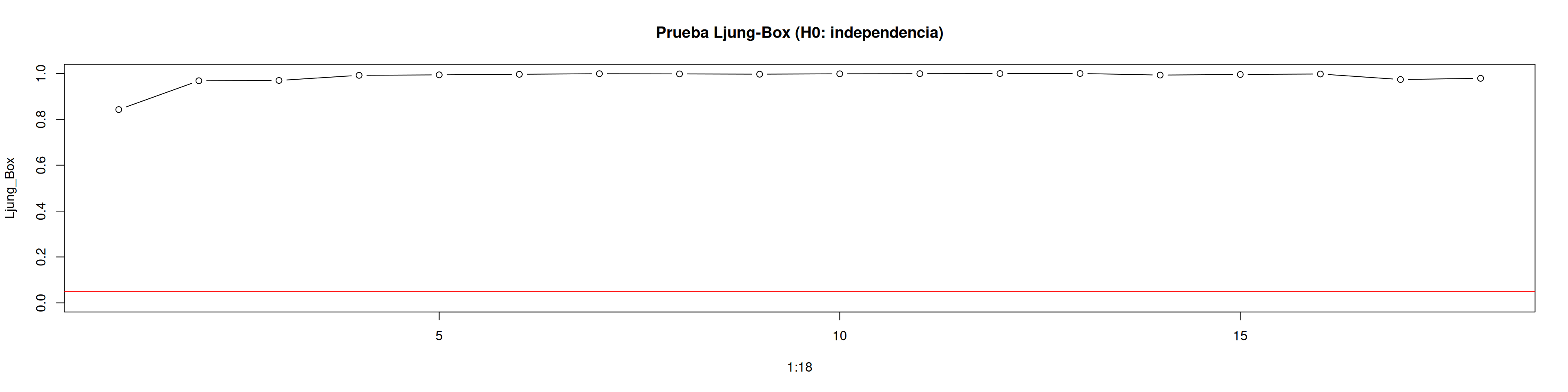

# Para varios rezagosLjung_Box <-sapply(1:18, function(i) Box.test(at_est, lag = i, type ="Ljung")$p.value)colnames(Ljung_Box) <-NULLdata.frame(Rezago =1:18, p.valor =round(Ljung_Box, 4))

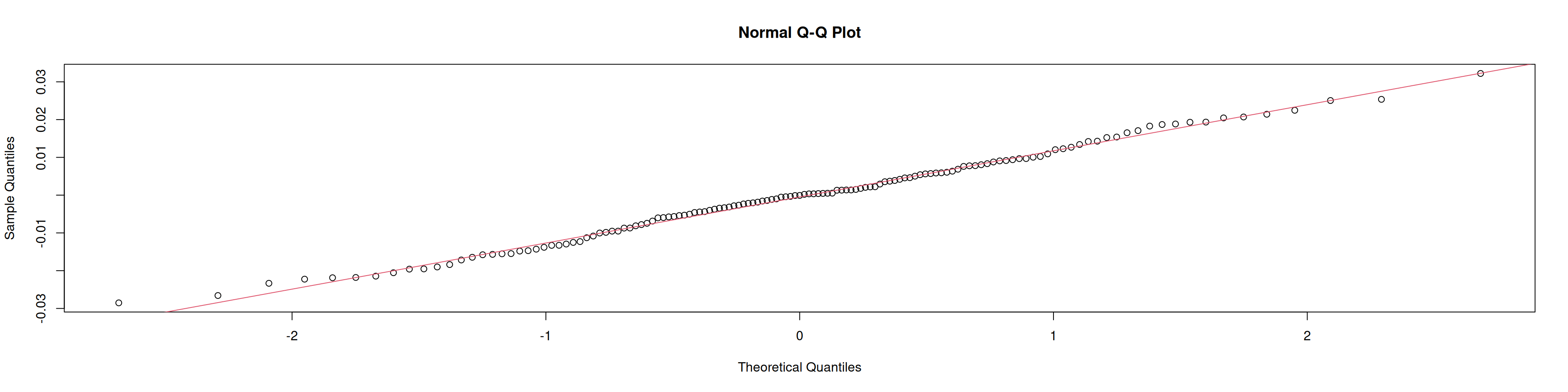

library(nortest)ad.test(at_est) # p-valor>0.05: no rechaza normalidad

Anderson-Darling normality test

data: at_est

A = 0.22546, p-value = 0.8166

shapiro.test(at_est) # idem

Shapiro-Wilk normality test

data: at_est

W = 0.99377, p-value = 0.8164

qqnorm(at_est); qqline(at_est, col =2)

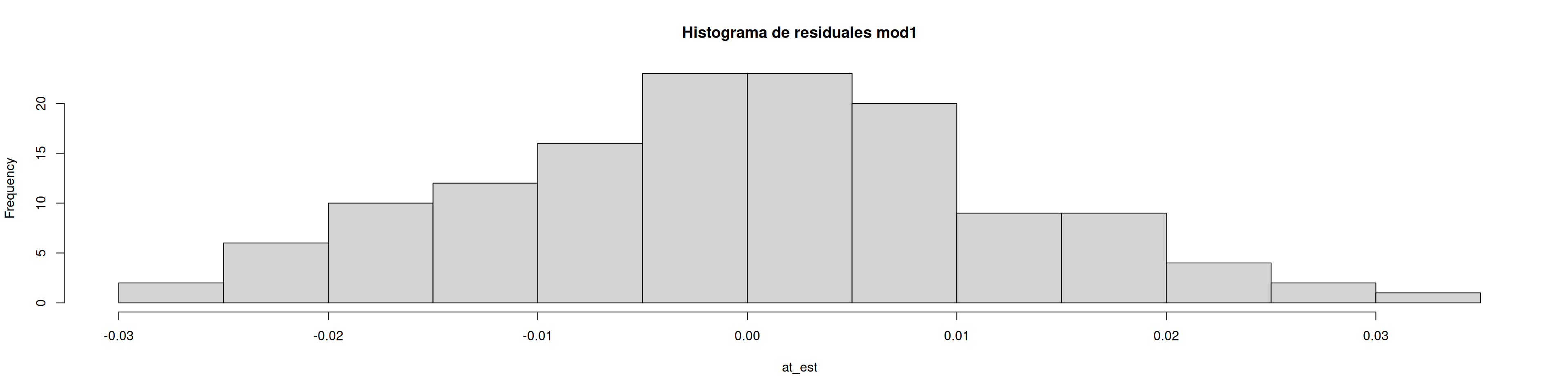

hist(at_est, main ="Histograma de residuales mod1")

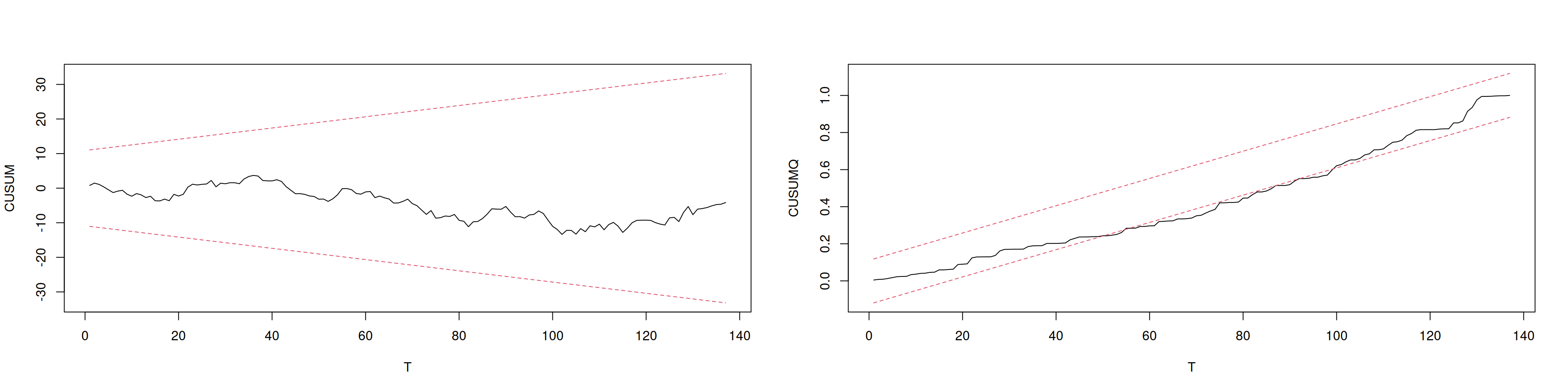

8.13 Función CUSUM y CUSUMQ

cucuq <-function(x, nivel) { A <-0.948 N <-length(x) T <-1:N cu <-cumsum(x) /sd(x) LS <- A *sqrt(N-1) +2*A*(T-1)/sqrt(N-1) LI <--LS cu2 <-cumsum(x^2) /sum(x^2) LS2 <- nivel + (T-1)/(N-1) LI2 <--nivel + (T-1)/(N-1)par(mfrow =c(1,2))matplot(T, cbind(cu, LS, LI), type="l", lty=c(1,2,2),ylab="CUSUM", col=c(1,2,2))matplot(T, cbind(cu2, LS2, LI2), type="l", lty=c(1,2,2),ylab="CUSUMQ", col=c(1,2,2))}cucuq(at_est, nivel =0.11848)

8.14 Evaluación predictiva dentro y fuera de muestra

# Dentro de muestrasummary(mod1)

Series: ytd

ARIMA(3,0,0) with zero mean

Coefficients:

ar1 ar2 ar3

0.5166 0.4765 -0.4043

s.e. 0.0772 0.0790 0.0774

sigma^2 = 0.0001495: log likelihood = 409.92

AIC=-811.84 AICc=-811.53 BIC=-800.16

Training set error measures:

ME RMSE MAE MPE MAPE MASE

Training set -0.0003684491 0.01209189 0.009562996 39.69704 126.5415 0.4781506

ACF1

Training set -0.01678247

summary(mod2)

Series: ytd

ARIMA(2,0,1) with zero mean

Coefficients:

ar1 ar2 ma1

-0.0941 0.6311 0.5533

s.e. 0.1002 0.0704 0.1114

sigma^2 = 0.000162: log likelihood = 404.55

AIC=-801.11 AICc=-800.81 BIC=-789.43

Training set error measures:

ME RMSE MAE MPE MAPE MASE

Training set -0.0002526163 0.01258662 0.01008932 37.02357 119.4948 0.5044668

ACF1

Training set 0.08053776

# Fuera de muestradatos.evalua <-read_excel("Programa_2_datos.xls", sheet ="Evaluar")yt.eval <-ts(datos.evalua[,2], start =c(2010, 12), frequency =12)mod1.evalua <-Arima(yt.eval, model = mod1)mod2.evalua <-Arima(yt.eval, model = mod2)accuracy(mod1.evalua)

ME RMSE MAE MPE MAPE MASE ACF1

Training set 39.11233 39.99697 39.11233 42.00275 42.00275 NaN -0.04246928

accuracy(mod2.evalua)

ME RMSE MAE MPE MAPE MASE ACF1

Training set 31.63266 33.46823 31.63266 34.05565 34.05565 NaN 0.1746239

---title: "ARMA - Box-Jenkins"author: "Brayan Cubides"toc: truetoc-location: righttoc-depth: 2#number-sections: truecode-tools: truelightbox: trueself-contained: false ---## Limpieza de entorno y carga de librerías```{r, fig.width=20, fig.height=5, out.width="100%"}rm(list =ls(all =TRUE))library(forecast)library(TSA)library(readxl)library(tseries)```## Definir directorio y leer datos```{r, fig.width=20, fig.height=5, out.width="100%"}# Cambiar "\" por "/" en la ruta#setwd("C:/Users/cubid/Desktop/QUARTO - MATERIAS UNAL/9 SERIES DE TIEMPO/Lesson04")# Leer datos desde Exceldatos <-read_excel("Programa_2_datos.xls", sheet ="Datos")```## Preparación de la serie y gráfica inicial```{r, fig.width=20, fig.height=5, out.width="100%"}yt <-ts(datos[,2], start =c(1998, 12), frequency =12)plot(yt, type ="l", main ="Serie yt", xlab ="Tiempo")```## Transformación logarítmica para estabilizar varianza```{r, fig.width=20, fig.height=5, out.width="100%"}ln.yt <-log(yt)plot(ln.yt, type ="l", main ="Serie en log", xlab ="Tiempo", ylim =c(3.5,5))```## Prueba de raíz unitaria (ADF)```{r, fig.width=20, fig.height=5, out.width="100%"}acf(ln.yt)adf.test(ln.yt) # Ho: no estacionaria, p-valor>0.05 => no rechaza Ho```## Primera diferencia para estacionariedad```{r, fig.width=20, fig.height=5, out.width="100%"}ytd <-diff(ln.yt, 1)mean(ytd)plot(ytd, type ="l", main ="Serie en primera diferencia", xlab ="Tiempo", ylim =c(-0.08,0.08))adf.test(ytd) # p-valor<0.05 => rechaza Ho```## Identificación: ACF y PACF```{r, fig.width=20, fig.height=5, out.width="100%"}par(mfrow =c(1,2))acf(ytd)pacf(ytd)```## Selección de modelo ARMA(p,q)```{r, fig.width=20, fig.height=5, out.width="100%"}eacf(ytd) # sugerencia ARMA(3,0)auto.arima(ytd, trace=TRUE)```## Estimación de dos modelos```{r, fig.width=20, fig.height=5, out.width="100%"}mod1 <-Arima(ytd, order =c(3,0,0), include.mean =FALSE)summary(mod1)mod2 <-Arima(ytd, order =c(2,0,1), include.mean =FALSE)summary(mod2)```## Diagnóstico del modelo 1```{r, fig.width=20, fig.height=5, out.width="100%"}at_est <-residuals(mod1)# Residuales y residuales estandarizadosplot(at_est, ylim =c(-0.1,0.1), main ="Residuales de mod1"); abline(h=0)par(mfrow =c(3,1))plot(rstandard(mod1), type ="o", ylab ="Residuales estandarizados"); abline(h =c(-2,0,2))acf(at_est, lag.max =36)pacf(at_est, lag.max =36)```## Prueba de Ljung-Box```{r, fig.width=20, fig.height=5, out.width="100%"}# Para varios rezagosLjung_Box <-sapply(1:18, function(i) Box.test(at_est, lag = i, type ="Ljung")$p.value)colnames(Ljung_Box) <-NULLdata.frame(Rezago =1:18, p.valor =round(Ljung_Box, 4))plot(1:18, Ljung_Box, type="b", main="Prueba Ljung-Box (H0: independencia)", ylim=c(0,1))abline(h =0.05, col ="red")``````{r, fig.width=20, fig.height=5, out.width="100%"}# tsdiag hace diagnóstico completotsdiag(mod1)```## Normalidad de residuales```{r, fig.width=20, fig.height=5, out.width="100%"}library(nortest)ad.test(at_est) # p-valor>0.05: no rechaza normalidadshapiro.test(at_est) # idemqqnorm(at_est); qqline(at_est, col =2)hist(at_est, main ="Histograma de residuales mod1")```## Función CUSUM y CUSUMQ```{r, fig.width=20, fig.height=5, out.width="100%"}cucuq <-function(x, nivel) { A <-0.948 N <-length(x) T <-1:N cu <-cumsum(x) /sd(x) LS <- A *sqrt(N-1) +2*A*(T-1)/sqrt(N-1) LI <--LS cu2 <-cumsum(x^2) /sum(x^2) LS2 <- nivel + (T-1)/(N-1) LI2 <--nivel + (T-1)/(N-1)par(mfrow =c(1,2))matplot(T, cbind(cu, LS, LI), type="l", lty=c(1,2,2),ylab="CUSUM", col=c(1,2,2))matplot(T, cbind(cu2, LS2, LI2), type="l", lty=c(1,2,2),ylab="CUSUMQ", col=c(1,2,2))}cucuq(at_est, nivel =0.11848)```## Evaluación predictiva dentro y fuera de muestra```{r, fig.width=20, fig.height=5, out.width="100%"}# Dentro de muestrasummary(mod1)summary(mod2)# Fuera de muestradatos.evalua <-read_excel("Programa_2_datos.xls", sheet ="Evaluar")yt.eval <-ts(datos.evalua[,2], start =c(2010, 12), frequency =12)mod1.evalua <-Arima(yt.eval, model = mod1)mod2.evalua <-Arima(yt.eval, model = mod2)accuracy(mod1.evalua)accuracy(mod2.evalua)```## Pronósticos con ggplot2```{r, fig.width=20, fig.height=5, out.width="100%"}library(ggplot2)library(forecast)# Pronóstico de diferenciasytd %>%Arima(order =c(3,0,0), include.mean =FALSE) %>%forecast(h =20) %>%autoplot()# Pronóstico en nivelesln.yt %>%Arima(order =c(3,1,0), include.mean =FALSE) %>%forecast(h =20) %>%autoplot()```